Why You Fail to Save Money Without Self-Discipline (Powerful Financial Psychology) is about understanding how self-discipline and self-control shape everyday money management in the American lifestyle finance. Many people want Financial success, Financial independence, and Financial freedom, but they struggle because of impulse spending, marketing influence, and spending temptation from online shopping ads and sales offers.

This article will explain how Financial planning, Budget control, and Financial discipline help create good savings habits and support long term wealth and wealth-building psychology. Readers will learn how Personal finance choices affect Financial security, Financial wellness, and Future security planning for life stability.

Why Self-Discipline Is the Psychology Behind Successful Saving

Saving money starts in the mind before it starts in the bank account. Self-discipline is closely connected to money psychology and Behavioral finance behavior patterns in Personal finance management. People who become good savers usually practice Financial discipline and strong self-control when making spending decisions. In the United States, research from financial education studies shows that about 63% of Americans do not have enough emergency savings for unexpected Financial emergencies, which creates Financial anxiety and weak Financial security. Financial success depends on Money control and Emotional spending awareness.

Self-discipline supports Smart spending, Budget tracking, and Expense control by helping people separate spending priorities from emotional desires. When people practice Financial literacy and Money education, they improve their Financial mindset and develop Wealth mindset habits that support Savings strategy and Savings growth. Financial responsibility grows when Personal responsibility is applied to Career finance, Household finance, and Personal budgeting decisions.

How Self-Discipline Controls Emotional Buying Decisions

Emotional buying behavior is strongly connected to Money psychology and Consumer behavior patterns influenced by Sales psychology and Marketing influence. When people experience Emotional spending, they often purchase items because of Lifestyle choices or social comparison pressure rather than real needs. Studies from consumer finance research show that nearly 40% of purchases in America are impulse spending-related.

Self-control helps control Emotional spending by creating Financial control over Lifestyle finance decisions. People who follow Financial success tips often apply Daily saving habits, such as saving money before spending money. The common rule among good savers isto saveg firstspendnd later.

Online shopping platforms increase spending temptation because of easy access to credit cards and buy now, pay later offers. Self-mastery finance techniques help people pause and evaluate Financial decisions before completing purchases. Good financial education teaches people to track Monthly budgeting goals and maintain Consistent saving patterns.

Why You Fail to Save Money Without Self-Discipline in Modern Consumer Culture

Modern consumer culture promotes Financial habits that encourage immediate satisfaction. Advertising, social media, and Lifestyle finance marketing encourage people to spend instead of saving. American consumer behavior studies show that adults see thousands of marketing messages daily, influencing Money priorities. This creates pressure to follow Lifestyle choices that may hurt Financial stability and Wealth accumulation goals.

Financial planning experts show thata lack of self-discipline leads to weak Savings habits and weak Financial responsibility behavior. People who practice Financial planning and Financial education tend to show stronger Wealth protection behavior. Financial stability requires long term saving consistency and Passive wealth creation strategies.

Financial security improves when individuals avoid Debt control problems and focus on Financial independence planning. Consumer psychology shows that Sales pressure during seasonal offers increases Emotional spending behavior.

How Advertising and Social Pressure Destroy Saving Habits

Advertising uses Sales psychology techniques such as scarcity marketing, social proof, and urgency messages. These tactics increase Spending decisions influenced by fear of missing out. Marketing influence is especially powerful in online shopping environments where Sales offers appear constantly.

Statistics from Global Consumer Finance Research show that:

- About 70% of millennials report that social media affects their Spending habits.

- Lifestyle finance pressure increases Luxury spending even when income management is weak.

| Marketing Trigger | Psychological Effect |

| Limited-time offers | Fear of missing out |

| Discount promotions | False savings perception |

| Influencer lifestyle ads | Social comparison spending |

Financial education programs teach Money control and Budget lifestyle planning to reduce these effects.

How Self-Discipline Helps You Stop Impulse Spending Immediately

Impulse spending is one of the biggest threats to Savings strategy success. When people lack Financial discipline, they spend money on Emotional spending triggers rather than Financial goals. Smart financial choices require strong self-control over daily spending decisions. Research shows Americans lose billions annually through impulse shopping behavior.

Impulse spending directly harms Financial wellness and Financial cushion building for emergencies. Good savers practice Financial responsibility by tracking Expenses and monitoring Cash management.

Practical Methods to Kill Impulse Purchases in Daily Life

People can improve Financial control by using practical behavioral finance techniques. One popular method is the 24-hour purchase rule, where consumers wait before buying non-essential products. This helps reduce Emotional spending and strengthens Financial mindset training.

Another strategy is removing stored credit card information from Online shopping websites. This reduces Credit card debt risk and supports Debt control habits.

Table of Practical Control Methods

| Method | Financial Benefit |

| 24-hour waiting rule | Reduces impulse spending |

| Cash payment usage | Improves Money control |

| Shopping list planning | Supports Budget tracking |

Studies show cash-based buyers spend about 25% less than credit users, according to financial behavior research.

Why Self-Discipline Is the Key to Becoming a Good Saver Over Time

Long term saving requires Financial discipline and Financial patience. Wealth building does not happen quickly, but through Consistent saving behavior and Savings habits repetition. Americans who maintain consistent savings for 20 years typically accumulate more wealth compared to inconsistent savers.

Financial success requires Financial planning for Future planning and Life planning goals. Career finance growth also contributes to Wealth discipline improvement.

The Role of Patience in Long-Term Wealth Growth

Patience supports long-term wealth creation through compound interest investments. Compound interest is powerful for wealth-building psychology because money grows using Passive wealth methods.

Example:

If $1000 is invested with 7% annual return:

- After 10 years → about $1967

- After 30 years → about $7612

| Time Period | Wealth Growth Result |

| 10 years | Moderate growth |

| 20 years | Strong growth |

| 30 years | Passive wealth accumulation |

Federal Reserve data shows disciplined investors have stronger Financial security and Economic security outcomes.

“Smart planners often study Financial Tricks Roarleveraging:Ultimate Expert Guide to learn advanced strategies that improve savings discipline and financial goal planning.”

How Self-Discipline Helps You Build Wealth Slowly but Surely

Wealth accumulation works best when people focus on Stable finance and Financial stability building instead of risky speculation. Smart investment requires Investment discipline and Smart investment strategy development. People with strong Financial wellness habits usually grow wealth gradually.

Passive wealth income streams, such as dividend investing and index funds,s help create long-term wealth security.

Compounding Savings and Financial Growth Psychology

Compound growth supports Savings growth because earnings generate more earnings. Behavioral finance research from Harvard financial studies shows disciplined investors outperform emotional traders by about 60% over long periods.

Self-discipline supports Investment discipline and Smart financial choices.

How Self-Discipline Helps You Achieve Financial Goals Faster

Financial goals provide direction for Financial success and Financial freedom planning. Goal setting helps improve Money priorities and Financial planning structure.

Studies from Dominican University show people who write financial goals are 42% more likely to achieve them.

Goal Visualization and Financial Planning Techniques

Financial visualization methods help improve Money psychology and Financial motivation. People can use vision boards or financial journals to track Financial success goals.

Financial goal formula:

Income management – Expense control = Savings investment amount

Regular Budget tracking improves Financial discipline and Financial responsibility performance.

Why You Fail to Save Money Because of Poor Financial Habits

Financial habits decide whether a person becomes a Good saver or struggles with Financial stability. Poor Financial habits develop when people repeatedly make bad spending decisions, ignore Budget control, and fail to practice self-discipline in Personal finance management. Financial habits are strongly connected to Lifestyle choices, Money priorities, and Career finance income behavior. According to financial behavior research, nearly 55% of Americans live paycheck to paycheck because of weak Financial planning and weak Financial responsibility awareness.

Spending habits usually grow from emotional Money psychology triggers. When people do not practice Financial literacy and Money education, they tend to prioritize emotional satisfaction over long term wealth protection. Wealth mindset development requires consistent Financial discipline, Daily saving habits, and Smart financial choices for future security planning. People who track Expenses and monitor Budget lifestyle patterns usually achieve stronger Financial success results. Financial wellness depends on building Positive habits around Money control and Cash management.

How Bad Spending Habits Form and How to Break Them

Bad spending habits usually develop through Consumer behavior patterns influenced by Marketing influence, Sales psychology, and Social pressure from peers. Online shopping and constant Sales offers encourage impulsive Financial decisions. Financial education experts say habit formation happens after repeated behavior cycles. If someone repeatedly practices Emotional spending, it becomes part of their Financial habits and Spending decisions.

Breaking bad habits requires replacing them with Positive financial behavior. For example, instead of spending on luxury products, individuals can redirect money toward Emergency savings or Investment discipline accounts. Research from behavioral finance studies shows that people who automate savings improve Savings consistency by nearly 50%.

Simple Habit Change Strategy Table:

| Old Habit | New Financial Habit |

| Emotional shopping | Budget tracking |

| Impulse buying | Savings strategy planning |

| Credit card dependence | Cash management |

Financial success tips recommend setting Monthly budgeting limits and using Financial planning apps to improve Money control and Financial control performance.

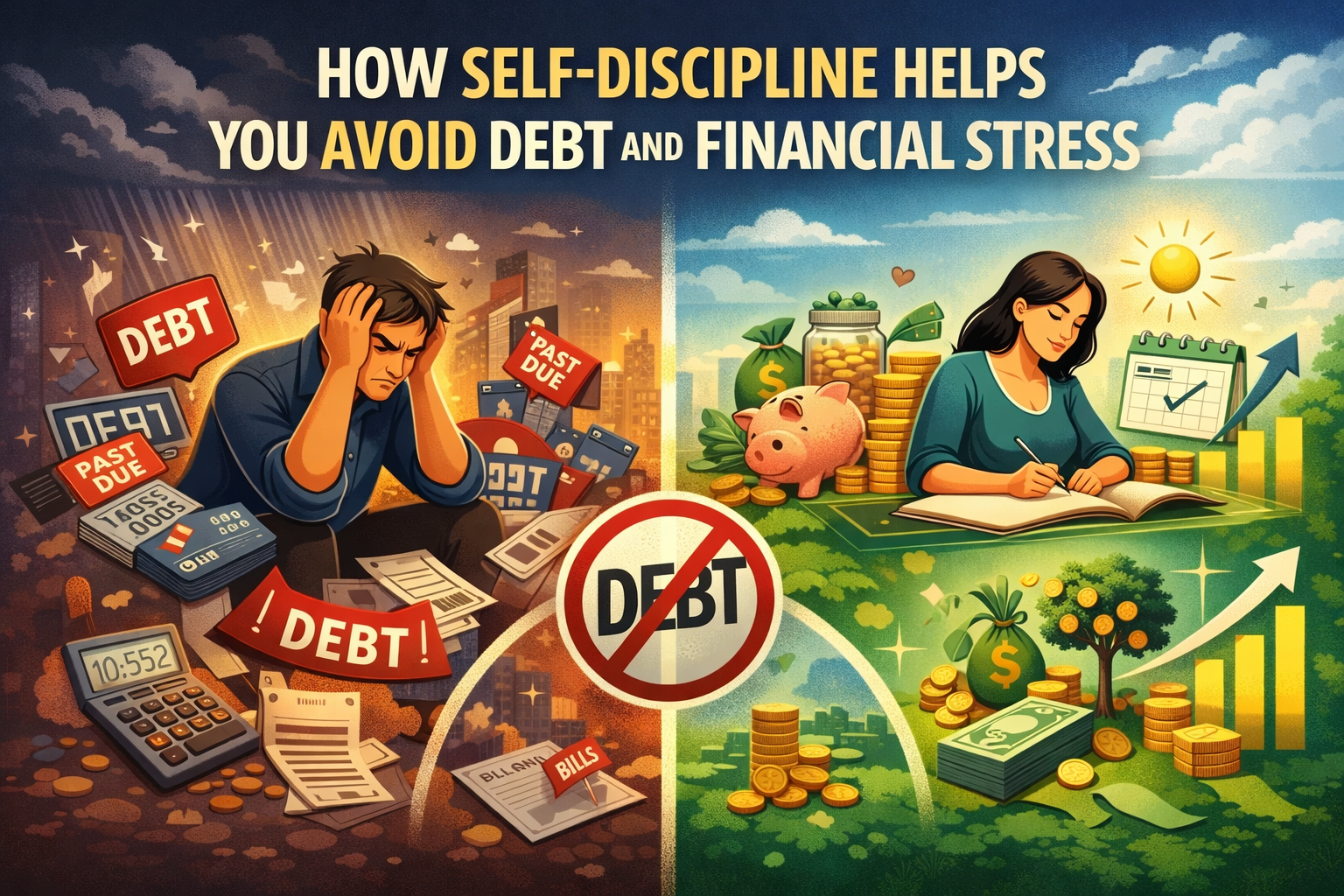

How Self-Discipline Helps You Avoid Debt and Financial Stress

Debt control is one of the most important parts of Financial security and Financial independence planning. Credit card debt and loan dependency can destroy Wealth protection and Financial cushion safety. In the United States, household debt reached over $17 trillion according to Federal Reserve economic reports. Debt pressure increases Financial anxiety and negatively affects Mental financial health.

Self-control helps people avoid unnecessary borrowing and supports Financial responsibility. Financial success depends on living within income management limits rather than spending future income today. Good financial behavior encourages saving money before spending money. People with strong Financial discipline usually maintain stronger Economic wellbeing and Financial wellness outcomes.

Credit Card Traps and Easy Credit Risks

Credit cards create convenience, but also create Credit card debt risk when used without Financial discipline. Minimum payment traps cause people to pay interest for years without reducingtheir principal balance. Average credit card interest rates in the United States range from 15% to 25%, which increases Financial stress and Money anxiety.

Credit Risk Prevention Tips:

- Pay the full balance monthly

- Avoid using credit for Lifestyle finance luxury purchases

- Use debt control payment plans

Financial education programs teach Smart spending and Financial planning behavior to reduce debt risks. Financial literacy improves Financial decisions and supports Money security goals.

Why Self-Control Is the Foundation of Financial Success

Financial success is not only about earning money but also about controlling money. Self control creates Financial discipline systems that support Financial stability, Wealth accumulation, and Financial independence. People with strong Self mastery finance skills usually make better Financial decisions during economic uncertainty.

Research from World Economic Studies shows that financially disciplined individuals report about 30% lower Financial stress compared to people with poor Money control habits. Financial success also improves Personal responsibility development and Financial wellness confidence.

Confidence and Financial Decision Making

Financial confidence grows when people practice good Money management. Financial control improves Mental financial health and reduces Financial anxiety. When people build Emergency savings funds, they feel safer during unexpected Financial emergencies such as medical bills or job loss.

Financial confidence-building methods include:

- Maintaining a financial cushion of savings

- Tracking Financial goals monthly

- Practicing Financial education learning

Confidence improves Smart financial choices because people feel comfortable making long-term financial planning decisions.

Developing Self-Discipline for Beginner Savers

Beginner savers must start with simple Financial discipline systems. Financial literacy education suggests starting small and gradually increasing Savings habits. Many Americans fail to save because they attempt complex investment strategies too early.

Good savers follow the Saving first, Spend later philosophy. This improves Financial responsibility and Wealth discipline behavior patterns. Financial planning should focus on income management and Expense control first.

Simple Daily Saving Rules for Beginners

Beginner saving success depends on consistent Daily saving habits. Experts recommend saving at least 10% of income for Financial security development.

Beginner Saving Plan Table:

| Income Level | Saving Percentage |

| Low income | 5–10% |

| Middle income | 15% |

| High income | 20–25% |

Simple Financial success tips include avoiding Lifestyle finance inflation and controlling Emotional spending habits. Beginners should focus on Budget tracking and Money control improvement before investing aggressively.

Advanced Saving Strategies for Financial Growth

Advanced savers focus on Financial automation, Investment discipline, and wealth-building psychology. Financial planning at an advanced level requires Smart investment diversification and Passive wealth creation.

Automation reduces human error in Financial decisions. Financial technology tools help maintain Consistent saving patterns.

Automation and Smart Saving Systems

Automated financial systems help maintain Financial discipline without constant manual effort. Many financial advisors suggest automatic transfers from checking accounts to savings accounts.

Advanced financial strategies include:

- Automatic investment contributions

- Index fund investment discipline

- Retirement planning contributions

Automation improves Savings growth and Financial success consistency. Financial security improves when people develop long-term saving habits.

Why Motivation Alone Fails Without Self-Discipline

Motivation is emotional, but Financial discipline is behavioral. Motivation may startwith financiall planning goals, but does not maintain consistent Financial success results. People often lose motivation after a few months of saving attempts.

Financial psychology research shows discipline-driven behavior creates stronger long term Financial success compared to motivation-based behavior.

Emotional vs Logical Money Management

| Emotional Money Management | Logical Money ManagementShort-term |

| m spending | Long-term saving |

| Emotional purchases | Planned financial decisions |

| Lifestyle pressure spending | Financial goal focus |

Financial mindset development requires balancing emotions and logic during Financial decisions.

Real-Life Financial Success Mindset of Good Savers

Good savers think differently about Wealth mindset and Money priorities. They focus on Financial freedom, Financial independence, and Wealth protection strategies. Good savers treat money as a tool for Future planning rather than short-term pleasure.

Financial success psychology research shows wealthy individuals prioritize Investment discipline and Savings strategy planning.

Rich vs Poor Spending Psychology Differences

| Wealth Mindset | Scarcity Mindset |

| Invest first | Spend first |

| Think long term | Think short term |

| Focus on Wealth building | Focus on survival spending |

Wealth accumulation requires consistent Financial discipline and Financial education knowledge development.

How to Recover Financially After Money Mistakes

Everyone makes Financial mistakes. Financial success depends on how quickly people recover from bad financial decisions. Financial discipline helps rebuild Financial control after financial losses.

Mistakes often happen due to Emotional spending or weak Financial planning systems.

Psychological Reset Strategies for Better Saving

Recovery strategies include:

- Stop guilt spending behavior

- Restart Budget control immediately

- Rebuild Savings habits gradually

Financial wellness improves when people accept mistakes as learning experiences. Financial literacy education supports Self improvement finance growth.

Self-Discipline as Your Long-Term Financial Superpower

Self-discipline works like a Financial success engine for long term Wealth building. Financial independence depends on Financial responsibility, Financial planning, and Investment discipline consistency. People who practice self-control usually achieve stronger Financial freedom outcomes.

Long term Financial success requires continuous Financial education and Money education learning. Wealth discipline protects against Financial emergencies and economic instability.

Future Financial Security Planning

Future planning should include:

- Retirement planning contributions

- Insurance financial protection

- Emergency savings funds

Financial security planning reduces Future financial stress and supports Life planning goals. Career finance stability also supports Household finance security.

“For deeper insights, explore Ultimate Guide: What Is Advice in Financial Planning RoarLeveraging in 2026 to understand expert strategies for smarter wealth planning.”

Frequently Asked Questions (FAQs)

Why is self-discipline important for saving money?

Self-discipline is important because it helps people control emotional spending and make smarter financial decisions. When someone practices self-control, they can focus on financial goals instead of buying things they do not need. This improves financial success, money control, and long-term wealth building. Without self-discipline, impulse spending, and lifestyle finance pressure can quickly reduce savings.

How does self-control help reduce impulse spending?

Self-control helps people pause before buying something. Instead of buying based on emotions or marketing influence from online shopping ads, people can ask if the purchase supports their financial goals. This simple habit lowers emotional spending, improves budget control, and supports savings consistency.

What is the connection between financial success and saving habits?

Financial success is closely linked to good saving habits. People who save regularly usually have stronger financial security and financial independence. Financial success does not only depend on income growth but also on smart financial choices and financial planning behavior.

How can I start saving money if I have a low income?

Start by saving a small percentage of income, even if it is 5% weekly or monthly. Focus on daily saving habits instead of large investments. Pay yourself first before spending on lifestyle choices. This helps build a financial cushion and emergency savings protection.

Why do people fail to save money even when they earn a good income?

Many people fail because of poor financial habits, lifestyle finance inflation, and emotional spending psychology. Higher income often leads to higher spending decisions. Without financial discipline and money control, income growth does not automatically create wealth accumulation.

How does marketing influence spending behavior?

Marketing influence uses sales psychology and sales pressure techniques like limited offers and discounts. These tactics create spending temptation and fear of missing deals. People who practice financial literacy can better resist marketing pressure and focus on financial goals.

What are good financial habits for a good saver?

Good savers usually practice budget tracking, expense control, and financial planning. They also follow saving first, spend later financial behavior. Consistent saving habits improve wealth mindset development and financial wellness.

How can I control credit card debt?

Pay full balances every month to avoid credit card debt interest. Avoid using credit cards for lifestyle luxury spending. Use cash management strategies for daily purchases. Credit control improves financial stability and financial security protection.

What is financial discipline?

Financial discipline is the ability to control money decisions using logic instead of emotions. It supports personal finance management, wealth protection, and financial success growth. People with strong financial discipline usually experience less money anxiety and better financial wellness.

How does financial planning help with saving money?

Financial planning helps organize income management, expenses, and savings strategy goals. People who plan their finances are more likely to achieve long-term wealth goals and financial freedom. Planning also supports future planning and life planning goals.

What is a wealth mindset?

A wealth mindset means thinking about money as a tool for building future security and passive wealth income. People with a wealth mindset focus on investment discipline, long-term wealth growth, and financial independence goals instead of short-term spending.

How does emotional spending hurt financial health?

Emotional spending happens when people buy things to feel better instead of meeting real needs. This behavior reduces savings growth and increases financial stress. Managing emotions improves money psychology and financial control.

Why is emergency savings important?

Emergency savings protect people from unexpected financial emergencies such as medical bills, job loss, or car repairs. Financial experts recommend keeping at least 3–6 months of living expenses saved for financial security.

How can I build long-term wealth slowly?

Long term wealth grows through consistent saving, smart investment, and financial responsibility. Investing in index funds, retirement accounts, and passive wealth opportunities helps build wealth over time.

What is financial freedom?

Financial freedom means having enough financial security to live comfortably without constant money stress. It happens when people achieve stable finances, wealth discipline, and financial independence through smart money management and consistent financial success habits.

Conclusion: Why Self-Discipline Is Essential for Wealth Creation

Why You Fail to Save Money Without Self-Discipline (Powerful Financial Psychology) can be answered simply: financial success depends on consistent behavior. Self-discipline, self-control, and Financial discipline build a wealth mindset, Financial stability, and Financial freedom. Saving money is not about income level but about Financial habits, Money control, and Financial responsibility decisions.

People who practice consistent saving, Financial planning, and Smart spending eventually achieve Financial independence and Economic security. Wealth creation is a long-term journey built on daily Financial discipline actions.

Disclaimer:

“This article is for educational and informational purposes only. It does not provide financial or personal advice. Financial decisions involve risk, and readers should evaluate their own financial situation or consult a professional before making financial decisions.”